Summary of Presidential Decree 95/26, of 22 May 2026

1. Object and Material Scope

• Purpose: The decree establishes the updated legal rules governing family financial assistance and benefits under Angola’s Compulsory Social Protection System.

• Covered Benefits: The material scope of this social protection explicitly encompasses three distinct cash benefits:

- Maternity Allowance (Subsídio de Maternidade)

- Nursing Allowance (Subsídio de Aleitamento)

- Family Allowance (Abono de Família)

2. Maternity Allowance

• Definition: The maternity allowance is a cash benefit granted to covered female workers. Its legal purpose is to fully compensate for the loss of salary resulting from a worker taking maternity leave or temporarily ceasing professional activities due to childbirth.

• Leave Duration and Timing

- Standard Leave: Female workers have a statutory right to 3 months of maternity leave around the time of childbirth.

- Pre-Partum Distribution: A worker may elect to begin her maternity leave up to 4 weeks before the expected date of delivery, with the remaining time utilized post-partum.

- Multiple Birth Extension: In the event of a multiple birth (twins, triplets, etc.), the

post-partum portion of the leave is legally extended by an additional 4 weeks.

• Pre-Maternity Leave

- High-Risk Legal Concept: “Pre-maternity leave” represents an independent period preceding standard maternity leave. It is granted if a high-risk pregnancy forces an early cessation of work.

- Medical Verification: To trigger this benefit, the condition must be certified by an

official medical expert belonging to the disability evaluation service (Serviço de

Avaliação e Verificação de Incapacidades – SAVI). - Maximum Duration: Pre-maternity leave begins on the exact date specified

by the SAVI medical expert and is strictly capped at a maximum of 180 days. - Compensation Level: During this pre-leave period, the worker receives a reduced

cash allowance equal to 60% of the standard maternity allowance calculation.

• Special Circumstances

- Delayed Births: If actual childbirth occurs later than the predicted medical date used

to start the leave, the leave duration is automatically increased to guarantee a full 9

weeks of post-partum rest.

• Pregnancy Loss & Child Mortality

- In cases of miscarriage, stillbirth, or immediate neo-natal death, the maternity

allowance is strictly limited to a flat 1 month compensation. - If a child passes away during an active standard maternity leave, the allowance is

terminated on the day the worker returns to work. However, for the specific month in

which she returns early, the maternity allowance must still be paid out in its full

monthly entirety.

• Qualifying Period and Financial Valuation

- Qualifying Period (Prazo de Garantia): To access the maternity allowance, a worker

must have accumulated at least 12 months of social security contributions

(consecutive or intermittent) within the last 36 months preceding the leave. - Value Calculation: The total maternity benefit equals 3 times the average of the

last 12 monthly base salaries declared to social security immediately prior to taking

leave. - Exclusions: Non-regular bonuses, holiday allowances (subsídio de férias), and

Christmas bonuses (subsídio de natal) are legally excluded from the calculation

baseline.

• Paternal Substitution Rights

The biological father has a statutory right to substitute the mother and claim the remaining maternity leave and cash benefits under two strict legal scenarios:

- Incapacity: Proven physical or mental incapacity of the mother, lasting for the duration of said incapacity.

- Death: The death of the mother during or shortly after childbirth.

• Employer Payment and Reimbursement Mechanism

- Direct Payment Deadline: For standard employed workers, the employer is legally obligated to advance the pre-maternity and maternity allowances via bank transfer to the worker’s account within 30 days from the start of the respective leave.

- Self-Employed & Unemployed Exception: If the mother is self-employed (trabalhadora por conta própria) or unemployed at the time of delivery, the Compulsory Social Protection System’s Managing Entity (Entidade Gestora) pays her directly.

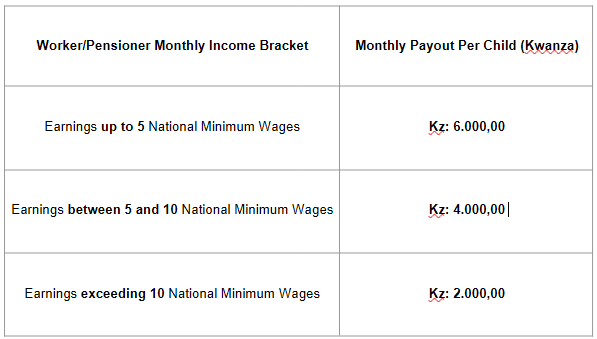

3. Nursing Allowance

• Definition: A cash benefit awarded directly to the child of a registered worker to offset the increased financial burdens of specialized early childhood nutrition.

• Qualifying Period: Requires at least 3 months of social security contributions (consecutive or intermittent) within the last 12 months preceding the claim.

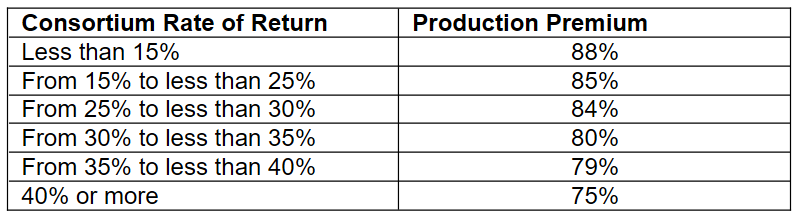

• Benefit Amounts Scaled by Income: Applying positive differentiation, the monthly cash payout per child is fixed based on the parent’s wage tiers:

• Payment Structure and Execution

- Lump-Sum Frequency: The benefit is disbursed in 3 large annual installments, each representing a grouped 12-month value allocation (p. 5). The initial installment is paid the month following application approval; subsequent installments deploy during the same homologous month over the next two years.

- Administrative Burden: The social security Managing Entity bears sole operational responsibility for paying this benefit.

- Application Requirements: Claims must be filed electronically by a parent, tutor, or

the employer on behalf of the worker, requiring:- The child’s official birth certificate/registration.

- An updated, verified immunization card (cartão de vacinação).

• Suspension and Extinction Conditions

- Immunization Suspension: The allowance is immediately suspended if the employer or worker fails to submit electronic proof of compliance with the national vaccination calendar. Payment only resumes once proof is uploaded, provided the child is still under 36 months old.

• Permanent Termination: The nursing allowance permanently ends when:

- The child reaches 36 months (3 years) of age.

- The child passes away.

- The claim is discovered to involve errors, simulations, or outright fraud.

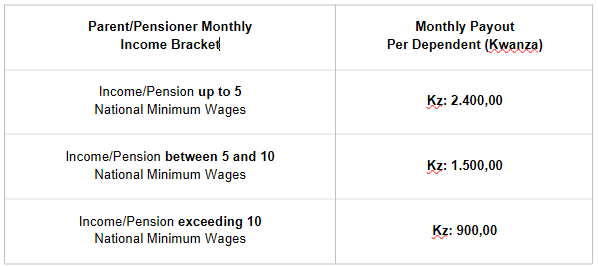

4. Family Allowance

• Core Concept and General Conditions

The family allowance provides continuous financial support to compensate for the ongoing costs of educating and raising children (p. 6). It is accessible to active workers, old-age pensioners (pensionistas de velhice), and absolute disability pensioners (invalidez absoluta).

To qualify and maintain access, five strict criteria must be met:

- The child must hold an official birth registration.

- The child must be formally registered as a dependent with the social security portal.

- The child must maintain an updated vaccination record.

- School-aged children must be enrolled in an official public or private school, proving

satisfactory academic progress (defined as passing and transitioning to the next

grade) each year. - Disabled children incapable of standard schooling must possess a certified disability

document verified by the SAVI medical board.

• Benefit Amounts Scaled by Income

The monthly allowance per dependent is stratified across three reference tiers:

• Payment Splitting and Boundaries

- Operational Division: Employers pay the allowance directly to active workers (clearly itemized on monthly payslips). The social security Managing Entity pays pensioners concurrently with their monthly pension disbursements.

- Dual-Income Household Splitting: If both parents are active workers, the responsibility for paying the child’s corresponding family allowance is split proportionally between their respective employers.

- Death Contingency: If the primary worker or pensioner dies, the benefit transfers to the surviving children and is paid alongside their official survivor’s pension (pensão de sobrevivência).

- Age Window & Cap: This specific allowance is requested starting from the 37th month of life (continuing seamlessly from where the nursing allowance ends). Claims are capped at a maximum of 5 children per worker.

• Suspension and Permanent Extinction

- Annual Verification Suspension: Beneficiaries must upload annual proof of schooling, academic progression, and vaccination during the first quarter (Q1) of every calendar year. Failure to do so triggers an immediate benefit suspension. If the documentation is submitted late, payments resume the following month, but the beneficiary forfeits all back-pay for the suspended months.

• Permanent Extinction: The family allowance permanently terminates if:

- The dependent reaches 216 months (18 years) of age.

- The suspension period hits an unresolved 24 consecutive months.

- The dependent fails to achieve academic grade progression for two consecutive years.

- The dependent registers as an independent worker and connects to an employer.

- The dependent passes away, or fraud is uncovered.

• Fraud Penalty: Any fraudulent collection of funds obligates the beneficiary to fully return all values, without prejudice to separate criminal prosecution.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}